Medicare Supplement Plans (Medigap) Explained for 2026

Medicare Supplement Insurance—also called Medigap—is designed to help pay the out-of-pocket costs that Original Medicare (Part A and Part B) does not cover. These costs can include deductibles, coinsurance, and copayments.

Medigap plans are standardized by the federal government, meaning each plan letter (A–N) offers the same core benefits no matter which insurance company you choose. The difference is the price, customer service, and underwriting—not the benefits.

What Medicare Supplement Plans Do

Original Medicare typically covers about 80% of approved Part B medical services, leaving you responsible for the remaining 20% plus other potential costs.

A Medicare Supplement plan helps reduce or eliminate those gaps, including:

- Hospital costs (Part A)

- Doctor visits and outpatient care (Part B)

- Skilled nursing coinsurance

- Blood (first 3 pints)

- Hospice coinsurance

- Foreign travel emergency (on most plans)

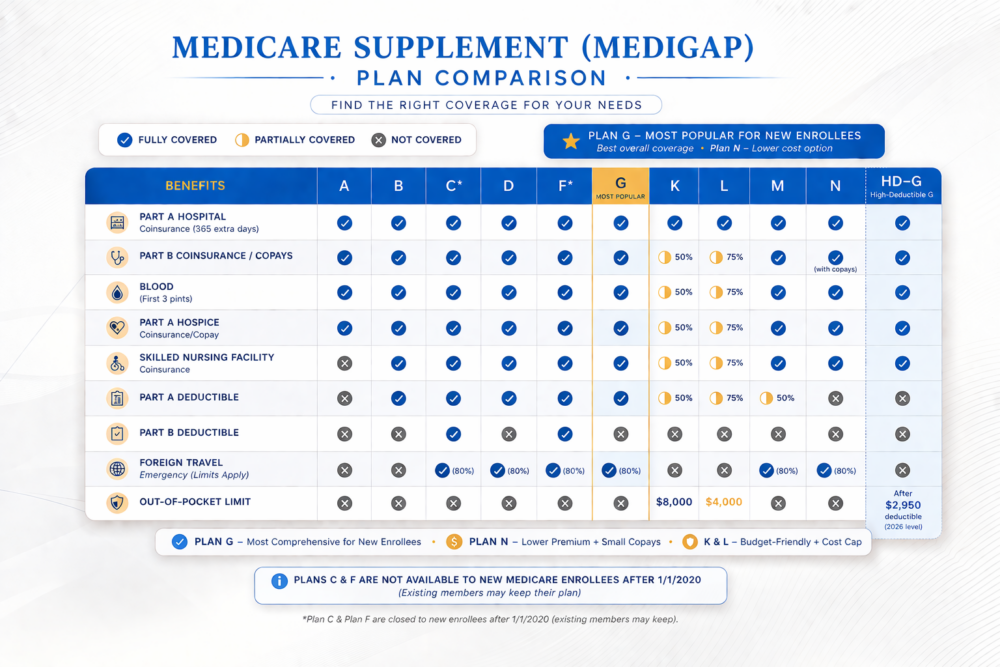

Medicare Supplement (Medigap) Plan Comparison – 2026

Coverage Overview by Plan (A–N + High Deductible G)

| Plan | Hospital (Part A) | Medical (Part B) | Part B Deductible | Part B Excess Charges | Foreign Travel | Cost Structure | Best For |

|---|---|---|---|---|---|---|---|

| A | Basic | Basic | No | No | Limited | Lowest coverage | Lowest-cost option |

| B | Yes | Yes | Yes | No | Limited | Low premium | Basic protection |

| C | Yes | Yes | Yes | No | Yes | Closed to new enrollees | Pre-2020 only |

| D | Yes | Yes | No | No | Yes | Moderate | Balanced coverage |

| F | Full | Full | Yes | Yes | Yes | Not available to new enrollees | Legacy only |

| G ⭐ | Full | Full | No | Yes | Yes | Moderate–High | Most popular for new enrollees |

| K | 50% | 50% | 50% | No | 50% | Low premium | Budget option |

| L | 75% | 75% | 75% | No | 75% | Low–Moderate | Mid-level coverage |

| M | Full | Full | 50% Part A | No | Yes | Moderate | Lower premium option |

| N ⭐ | Full | Copays apply | No | No | Yes | Lower premium | Cost-conscious users |

| High-Deductible G ⭐ | Full | Full after deductible | Yes (high deductible) | Yes | Yes | Lowest premium | Lowest monthly cost strategy |

Quick Plan Highlights

Plan G – Most Complete Coverage

- Pays almost all Medicare gaps

- No Part B deductible

- Predictable healthcare costs

Plan N – Balanced Savings

- Lower premium than G

- Small copays for doctor & ER visits

- No Part B excess charges coverage

High-Deductible G – Lowest Premium Strategy

- Very low monthly cost

- You pay Medicare-approved costs until deductible is met

- Full coverage after deductible

How to Use This Chart

- Lowest monthly cost: High-Deductible G or Plan N

- Most predictable coverage: Plan G

- Budget + moderate usage: Plan N or M

- Legacy enrollees: Plan F or C

How to Choose the Right Plan

- Your monthly budget

- Your healthcare usage

- Your comfort with copays/deductibles

- Travel needs

- Retirement income strategy

Important Medicare Supplement Facts

- Only works with Original Medicare (Part A & B)

- Does NOT include prescription drug coverage

- Standardized benefits nationwide

- Prices vary by company and location

Get Help Choosing the Right Plan

Medicare can feel overwhelming, but you don’t have to choose alone.

📞 Call today for a free Medicare Supplement comparison

We’ll help you compare plans side-by-side and find the best fit for your needs and budget.

👉 Speak with a licensed Medicare advisor now

Medicare Supplement plan comparison

Florida Medigap Insurance Policies for People Under Age 65 on Disability

Florida Medigap policies for people under age 65

are available for individuals eligible for Medicare due to a disability or End-Stage Renal Disease (ESRD).

You may be eligible for a Medicare Supplement policy before age 65 due to:

- a disability, or

- ESRD (permanent kidney failure requiring dialysis or a kidney transplant)

When Can I Enroll in a Medicare Supplement?

During your Medicare Initial Enrollment Period, which begins when you turn 65 and continues for 6 months,

you are entitled to enroll in any Medicare Supplement or Medigap policy. At this time, you cannot be turned

down or rated up due to pre-existing conditions. This is referred to as your Guarantee Issue Period.

During this period:

- You can buy Medicare Supplement/Medigap policies from private insurance companies available in your state

- Insurance companies can’t refuse to sell you a policy due to a disability

- They cannot charge you a higher premium because of your health status

- They cannot charge more than they charge other people age 65

At National Insurance Services of North America (NISONA), we are committed to your total satisfaction.

We offer a truly unbiased approach and practical solutions to help you find a plan that best fits your needs and budget.

Medicare is not one size fits all.

Give us a call and we will help you explore your options and answer any questions you may have. You are under no obligation.

Our goal: “Peace of mind to last you a lifetime!”

Nisona serves the insurance needs of the Treasure and Space Coast.